Q2 2026: What’s Behind the $3.2bn Rebound

African start-up funding has re-entered growth — but the capital coming back looks nothing like the capital that left in 2022. Five findings from the data.

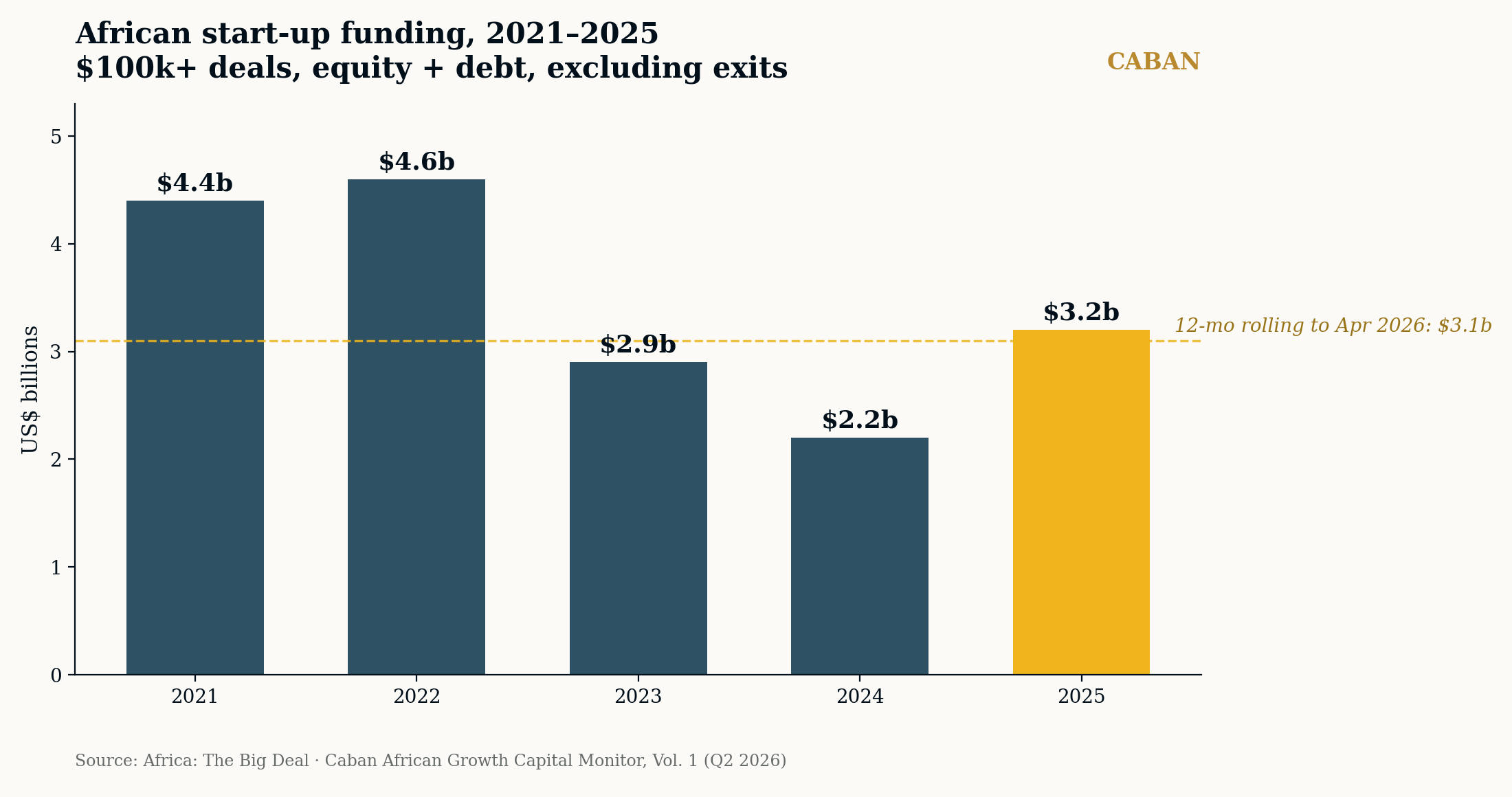

1. The headline: growth is back

African start-ups raised $3.2 billion in 2025 — up roughly 40% on 2024 and the first year-on-year growth in three years, according to Africa: The Big Deal's tracking of $100k+ deals. The trailing 12 months to April 2026 hold at $3.1 billion, confirming a market that has stabilised well above its 2024 floor of $2.2 billion, though still beneath the 2021–22 peak of $4.4–4.6 billion.

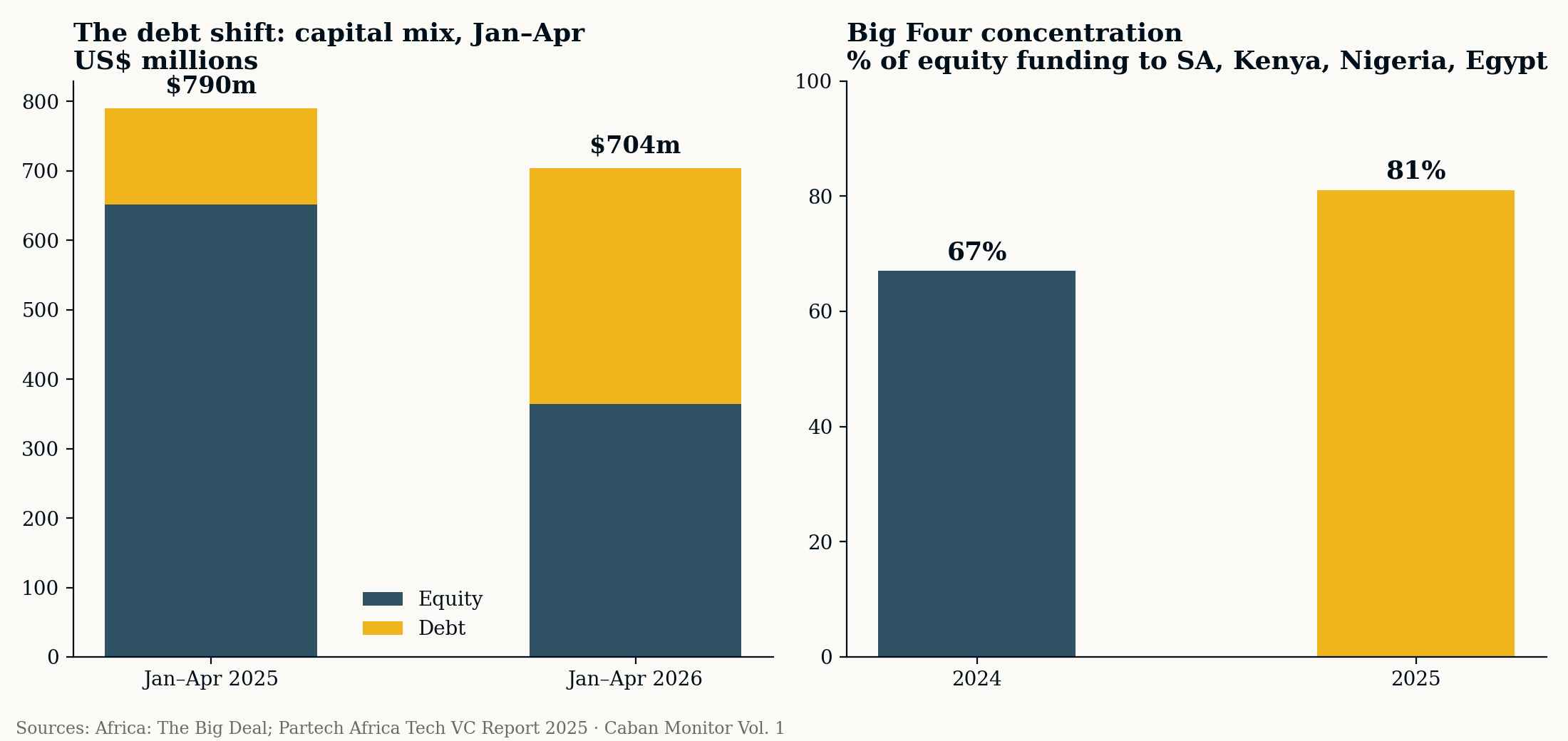

2. The composition: debt has arrived

The recovery's most important feature is invisible in the headline. In January–April 2026, debt made up 48% of all capital raised ($340m of $708m) — against just 17% in the same window of 2025. AVCA puts African venture debt at $1.8 billion for 2025, nearly double the prior year. Founders are financing growth without surrendering equity at reset valuations; capital providers are pricing African risk with instruments banks never offered this market.

3. The concentration: the Big Four pull away

South Africa, Kenya, Nigeria, and Egypt captured 81% of 2025 equity funding, up from 67% in 2024 (Partech). Capital is not returning evenly — it is returning to depth: markets with functioning exit routes, institutional co-investors, and governance infrastructure. For businesses outside the Big Four, the bar for preparation has risen, not fallen.

4. The exits: the window reopened

November 2025 delivered the continent's first significant tech IPOs in over six years — Optasia raising $345 million on the JSE at a $1.4 billion valuation, followed by Cash Plus in Casablanca. Exit proof is the single variable LPs have waited on; its return changes the fundraising conversation for every African growth company with listing-grade governance.

5. The capital base: Africa funds itself

African investors accounted for 45% of venture fund commitments in 2025, up from a 23% average across 2022–24 (AVCA) — led by DFIs, local corporates, and policy shifts such as Ghana's 5% pension allocation to VC and PE. A domestic capital base dampens the boom-bust cycle imported capital created.

What it means

For founders: the funding winter's lesson is permanent — investability is now a spectrum of financial hygiene, governance, and instrument-fit, not a pitch. Debt options reward exactly the preparation equity investors also price. Start with the readiness check.

For investors: concentration into the Big Four plus a reopened JSE window makes South African mid-market exposure the most exit-proximate allocation on the continent — and the reason our co-investment pipeline is weighted there.